V Trustees Limited (the Trustee) was concerned to protect the position of C who was the beneficiary of a trust much diminished due to the actions of her litigious brother, A, whose conduct had caused substantial losses with “no signs of the attacks abating.”

The matter came before the Jersey Royal Court on an application to bless decisions to remove A (and his spouse (considered further below)) as beneficiaries of two trusts.

As set out at [27] with respect to a prior Court of Appeal judgment:

“In its judgment the Royal Court noted, with considerable regret, the history of obstruction and misconceived litigation in which the Appellant (A) and [Mr E] had embroiled the trusts, causing huge wasted expenditure. It is hard not to sympathise with his siblings, who must watch with dismay their rapidly dwindling fortunes. Whatever justification the Appellant might have for any concern about the way in which the trusts have been or are being administered, this present appeal is a chapter in misguided and ruinous family litigation: this appeal, with all its attendant costs for the trusts, is not an appropriate occasion for investigating the Appellant’s concerns about the trusts’ administration.“

In declining to bless the removal decisions the Royal Court identified significant failings in the process adopted by the Trustee. These included:

- not making enquiries about A’s financial position. Although for an alternative view here see https://mattersoftrust.co.nz/2025/07/21/unfair-unprofessional-and-unfortunate/

- discuss the proposal with Mr A.

- “Even if the Trustee felt that a discussion with Mr A was not possible (which is not minuted), the Trustee did not even debate whether or not it was appropriate to explore its proposal with Mr A or adduce before us any evidence to explain why there was no discussion with Mr A.” [333(iv)]

- “While the Trustee has contended that it did not have to justify its change of position since 2020 when it was looking at an unequal allocation of assets, what the Trustee did not do was inform Mr A that it was considering looking at a total exclusion of Mr A and his issue.” [333(v)]

- failing to consider whether Mr A was married or had children. “While the Trustee sought to suggest that Mr A should have made the Trustee aware that he had got married in May 2023 and that W was expecting a child by the time of the First Decision (and had been born by the November 2023 Decision), for a decision of this significance, we consider that the onus was on the Trustee, given the duties owed by any trustee to beneficiaries, to ascertain whether there were any issue.” [333(vi)]

- the inference that the settlor’s wishes were not considered: While Mr Flavin indicated it was open to the Trustee to attach little weight to those wishes, it was not clear to us whether the Trustee did in fact do so: [333(vii]

- failing to follow advice. “… Mr Flavin correctly reminded the Trustee about the first part of paragraph 115 of the Court’s judgment in 2020; yet the Trustee only proceeded on the basis of paragraph 115(ii) and therefore failed to have regard to Mr Flavin’s advice“: [333(viii)]

- a quantitative analysis of loss, which while mathematically correct, could not be fully attributed to Mr A

- the Trustee’s failure to consider an unequal split – essentially favouring a quantitative assessment of loss ahead of a qualitative assessment of options available to the Trustee.

Notwithstanding the above the Royal Court was alive to the practical realities the Trustee confronted. As noted at [335]:

“… what we do accept is that Mr A will never be satisfied and will continue to ask questions. While some of those questions may be justified, a number of the assertions he made meant it was clear to us that Mr A would always be asking questions seeking information and challenging the Trustee’s decision. He will therefore always be putting the Trustee to significant cost and expense.”

While the decisions were not blessed (and there were cost consequences to the Trustee that flowed from this (see Representation of V Trustees Limited re N Trust [2025] JRC 200), the Royal Court did suggest a path forward in the following terms:

References:

- Representation of V Trustees Limited re N Trust [2025] JRC 188

- Representation of V Trustees Limited re N Trust [2025] JRC 200

- SG Kleinwort Hambros (C.I.) Limited [2023] JCA 088

- Representation of V Trustees Limited (Formerly G Trustees Limited) re K and N Trusts [2020] JRC 220.

- Representation of V Trustees Limited (formerly G Trustees re K and N Trusts) [2020] JRC 255.

- Kan v HSBC International Trustee Limited [2015] (1) JLR Note 31.

- Kan v HSBC International Trustee Limited [2015] JCA 109.

- Representation of Hawksford Trust re H Trust [2018] JRC 171.

- In the Matter of the R Trust [2019] SC (Bda) 36 Civ.

- Representation of GB Trustees Limited re Manor House Trust [2021] JRC 048.

- Eclairs Group Limited v JKX Oil and Gas Plc [2015] UKSC 71.

- Adams v FS Capital Limited [2023] EWHC 1649 (Ch).

- Crociani v Crociani [2014] JCA 089.

- HSBC International Limited v Poon [2014] JRC 254A.

- Representation of G Trustees Limited [2017] JRC 162A.

- In the Matter of the E Trust [2017] SC (BDA) 103 Civ.

- Representation of Otto Poon Trust [2015] JCA 109.

- In the matter of Vistra Corporate Services Ltd re: Ennismore Fund Management Limited Employee Benefit Trust [2023] JRC 222.

- Piedmont and Riviera Trusts [2021] 2 JLR 135.

- Representation of Z Trustee re A Family Settlement [2025] JRC 062

Discussion

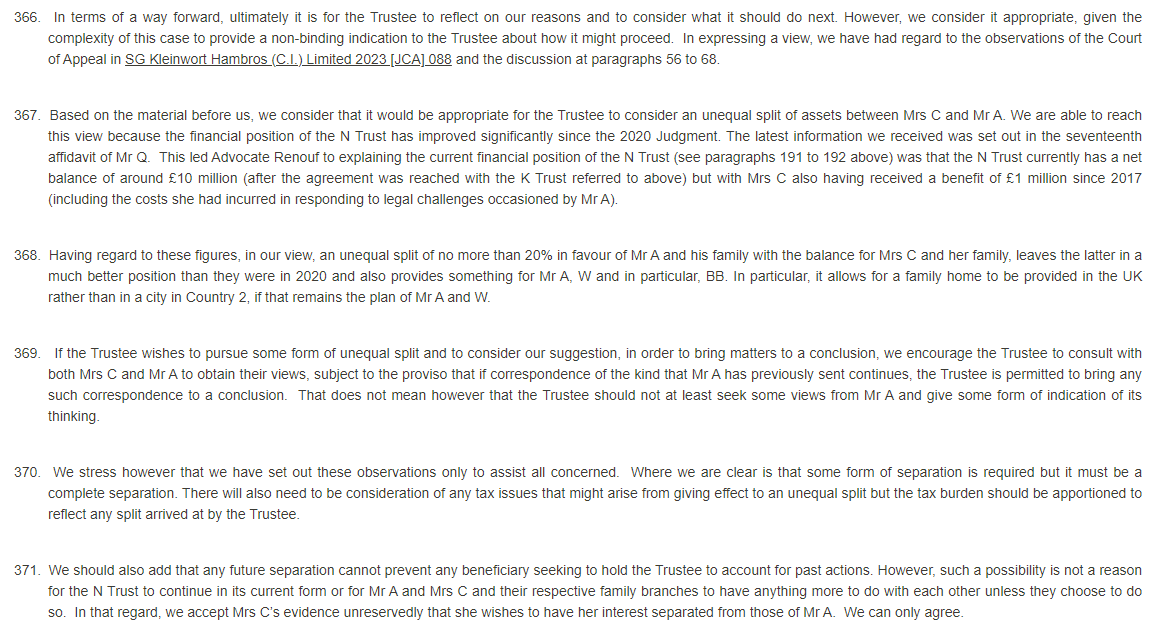

No comments yet.