In Estate of Twaites one of the will-maker’s son seeks a remedy under the Family Protection Act 1955 for a breach of the moral duty owed by his father to him. The Court was satisfied that there was a breach. However, before this could be quantified by way of an award in the son’s favour matters to determine included whether the estate included an advance from a trust that was wound up during the will-maker’s life and whether certain inter vivos gifts were Donationes Mortis Causa.

Trust advance

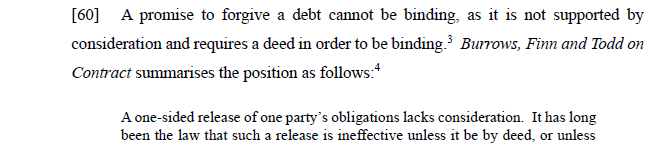

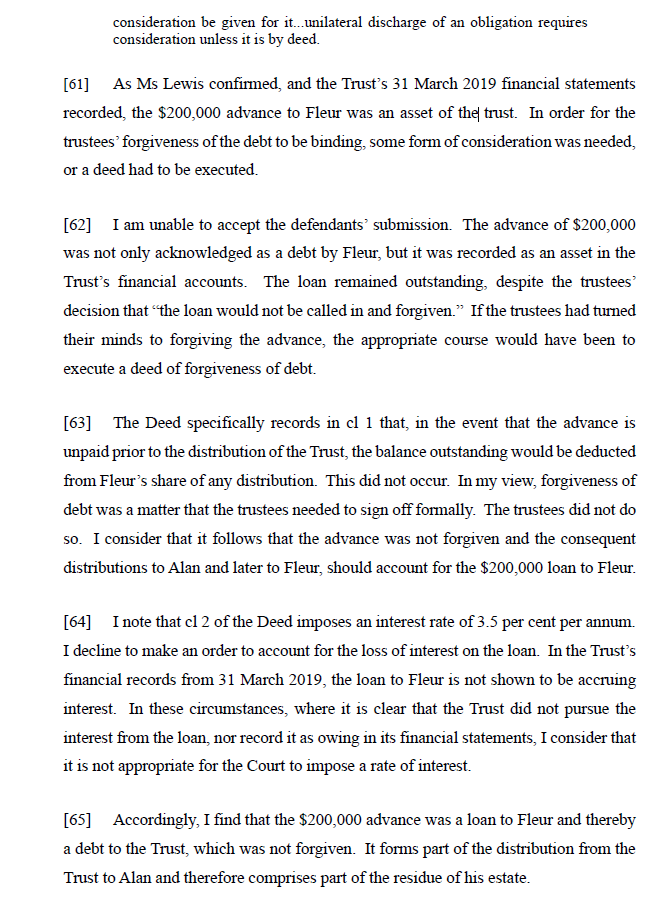

One of the will-maker’s children was advanced $200,000 from a trust prior to the trust being wound up. The advance was recorded in an acknowledgment of debt, although this only became apparent during the hearing. It was understood that the advance would be forgiven, or if distributed to the will-maker, would be forgiven in his will. This did not happen. As noted at [60] to [65]:

A cautionery tale.

Gifts donationes mortis causa

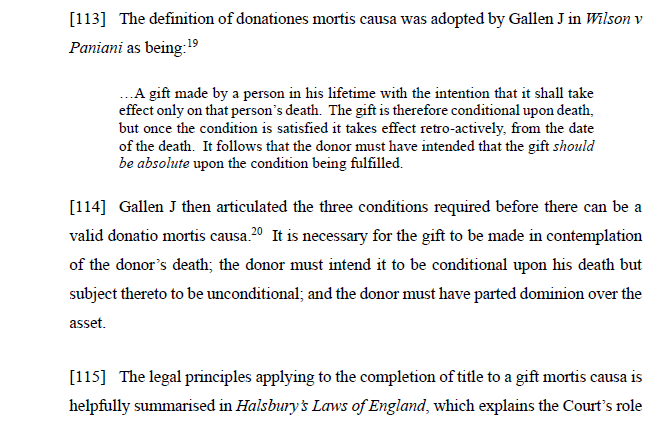

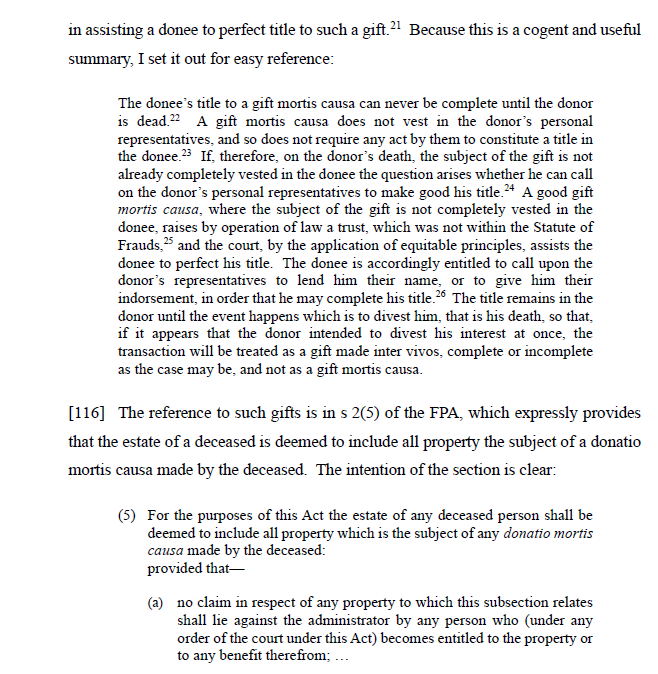

The significance of a gift beintg a gift that is donatio mortis causa is that the gift continues to comprise part of a will-maker’s estate for the purposes of the Family Protection Act 1955. Donationes mortis causa are discussed as follows at [113] to

The conditions required for a valid donatio mortis causa are a gift was made in contemplation of the donor’s death. The donor must intend it to be conditional upon death and all steps must be taken to part with the property. Once death occurs, the gift becomes unconditional.

Finding that certain gifts were not donationes mortis causa Cull J hedl that “Even though the gifts were made in contemplation of death, [the will-maker] parted with the moneys and did not make it conditional upon his death.”

References:

- Estate of Twaites [2025] NZHC 3998

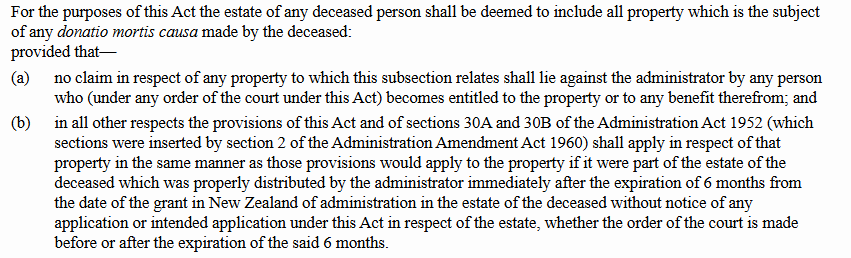

- Family Protection Act 1955, s 2(5):

Discussion

No comments yet.