In the matter of The Piedmont Trust and the Riviera Trust relates to an application for the Jersey Royal Court to approve the final distribution of trust assets in circumstances where the beneficiaries are in agreement regarding the termination of the trusts (but where there is disagreement regarding the allocation of the trust assets between the beneficiaries).

The Piedmont Trust was settled by deed dated 4 April 2000 at the instigation of the children beneficiaries’ father. The assets of this trust were valued at US$34.8m.

The Riviera Trust was settled by deed dated 18 June 2010. The beneficiaries of this trust were the beneficiaries of the Piedmont Trust together with the Riviera Trust’s settlor (who was related to the beneficiaries) and the father’s long-time companion. The assets of this trust were valued at US$7m.

There were three letters of wishes with respect to the Piedmont Trust and one with respect to the Riviera Trust. The letter of wishes with respect to the Riviera Trust is largely in line with the last letter of wishes with respect to the Piedmont Trust.

There was a background of family disharmony and appointments of protectors and trustees that were subsequently held to be invalid.

Wind up proposals were proposed by different beneficiaries.

Following the death of the father, the Trustees of each trust decided to consider the wind up afresh and invited submissions from the beneficiaries.

Agreement was reached in principle subject to protector approval, which was obtained. The Trustees then sought the approval of the Court. As noted at [31] “There is no dispute that termination of the Trusts in circumstances where there is strong disagreement amongst the beneficiaries is a momentous decision and that it is reasonable for the Trustees to seek the Court’s blessing.”

Tax consideration

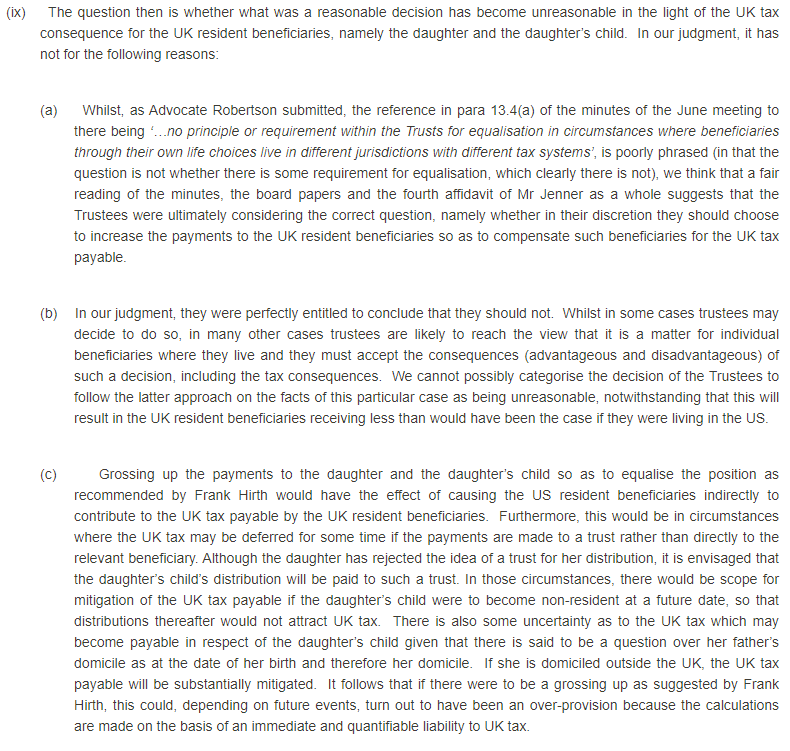

When the matter came before the court, as noted at [32]: “… the Trustees made it clear that they were approaching the matter in two stages. In stage 1, they were seeking the Court’s approval to the percentage split between the various beneficiaries as set out in the Proposed Distributions. Thereafter, in stage 2 the Trustees would work with individual beneficiaries to consider the tax position of each beneficiary and the best way in which that beneficiary’s distribution should be made, i.e. directly to a beneficiary, to a trust for the benefit of that beneficiary or in some other manner.”

Matters were adjourned so that the Trustees could get tax advice.

With respect to the proposed decision, the Court noted at [44] as follows:

Conflict of interest

Questions were then raised regarding alleged conflicts of interest. In this regard the Court noted as follows:

Letter of wishes

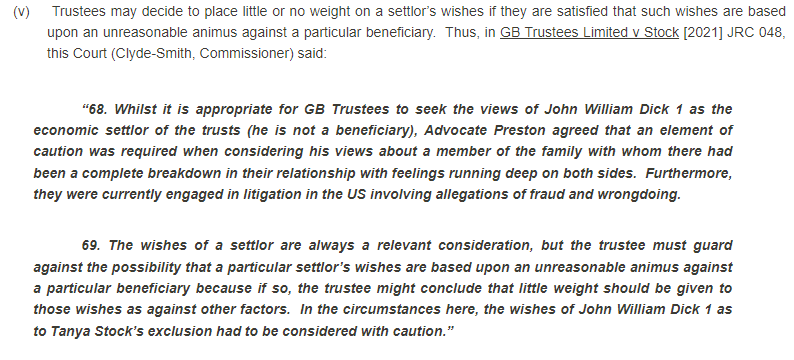

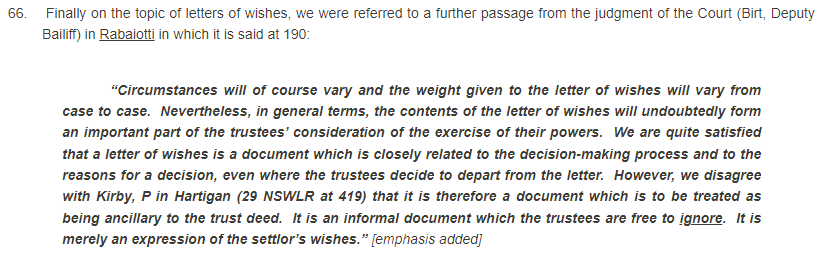

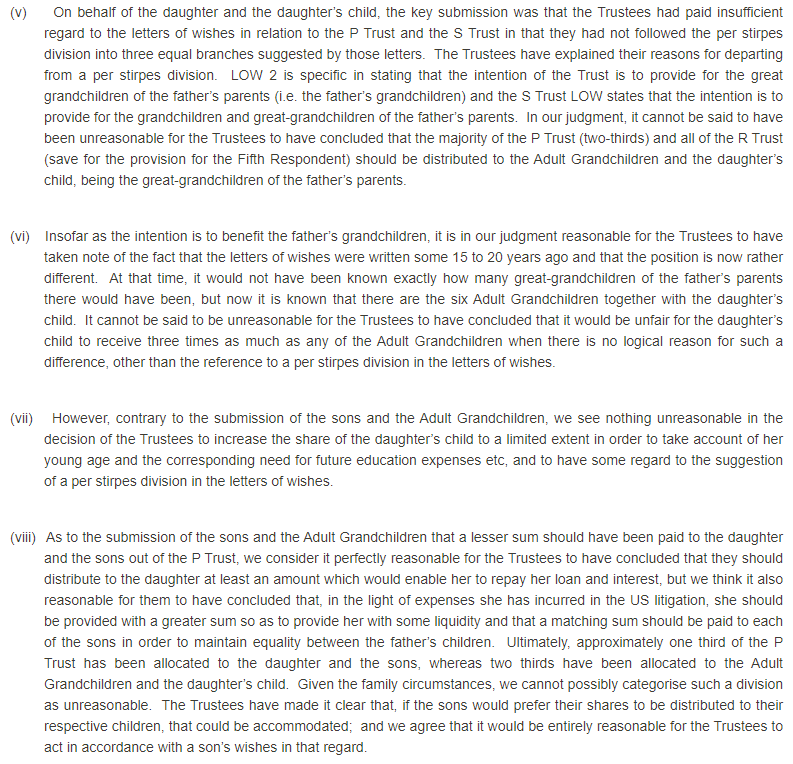

The next matter for the Court was whether the Trustees paid sufficient regard to the letters of wishes. As noted at [63]:

In a post script to the decision the Court further considered the role of protector (considered in Re the x Trusts), which is not a significant consideration in New Zealand (as a general observation).

The takeaway message is that Trustees have wide discretion on a pre-vesting date wind up. However, it is essential that a process is adopted. The process may be able to be challenged, and there might be better ones. It isn’t a contest between better and best; but rather can you explain why you did what you did?

References:

- In the matter of The Piedmont Trust and the Riviera Trust 05-Oct-2021

- In the matter of The Piedmont Trust and the Riviera Trust 06-Oct-2021

- Re Piedmont Trust, [2015] (2) JLR 52, [2015] JRC 196

- Re Piedmont Trust [2018] (2) JLR 306, [2018] JRC 210

- Re The X Trusts [2021] SC (Bva) 72 Civ

- Representation of Jemma Trust Company Limited re the V Trust 09-Sep-2022

Discussion

No comments yet.