Inland Revenue has issued a General Article (GA 24/01) providing guidance regarding how Inland Revenue might perceive certain transactions and structure changes.

In GA 24/01 Inland Revenue provides high level guidance regarding specific transactions and structural changes that are unlikely to be considered tax avoidance (without artificial or contrived features) such as distributions of income to a beneficiary on a lower tax rate than the trustee.

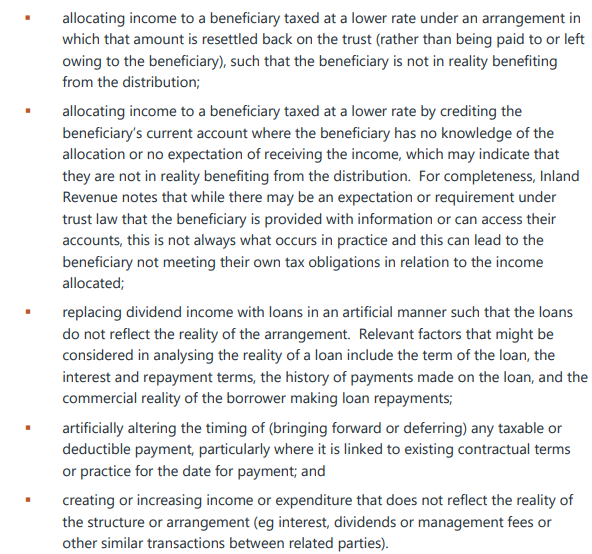

Helpfully, Inland Revenue also sets out situations where Inland Revenue may have concern or may need to enquire further. These are set out at 11 of GA 24/01 as follows:

As noted at [12]:

References:

- GA 24/01

- Interpretation Statement IS 23/01: Tax avoidance and the interpretation of the general anti-avoidance provisions in sections BG 1 and GA 1 of the Income Tax Act 2007

- Questions We’ve Been Asked QB 23/01: Income tax: scenarios on tax avoidance – 2023

- Questions We’ve Been Asked QB 23/02: Income tax: scenarios on tax avoidance – 2023 No 2

- Revenue Alert 21/01: Diverting personal services income by structuring revenue earning activities through a related entity such as a trading trust or a company sets out the circumstances in which Inland Revenue will consider this arrangement is tax avoidance.

- Revenue Alerts 18/01 and 18/01a: Dividend stripping and Questions and answers

- Interpretation Statement IS 24/01: Taxation of trusts explains the taxation oftrusts under the trust rules in the Income Tax Act 2007

Discussion

No comments yet.