The Minister of Revenue introduced the Taxation (Annual Rates for 2025–26, Compliance Simplification, and Remedial Measures) Bill (the Bill) into the House on 26 August 2025.

Amongst other things the Bill proposes:

- to repeal specific provisions for trust disclosure in sections 59BA and 59BAB of the Tax Administration Act 1994 (TAA) as these are not necessaray for the Commissioner to collect information from trustees pursuant to sections 33 and 35 of the TAA. As noted in the Bill Commentary on p 98:

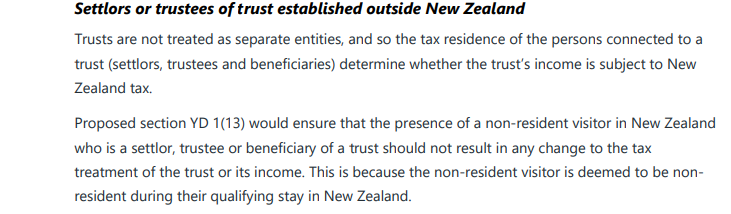

- an amendment that would ensure that entities associated with a non-resident visitor will not be considered when determining whether the entity is New Zealand tax resident or the entity’sincome is subject to New Zealand tax obligations. As noted at page 28 of the Bill Commentary:

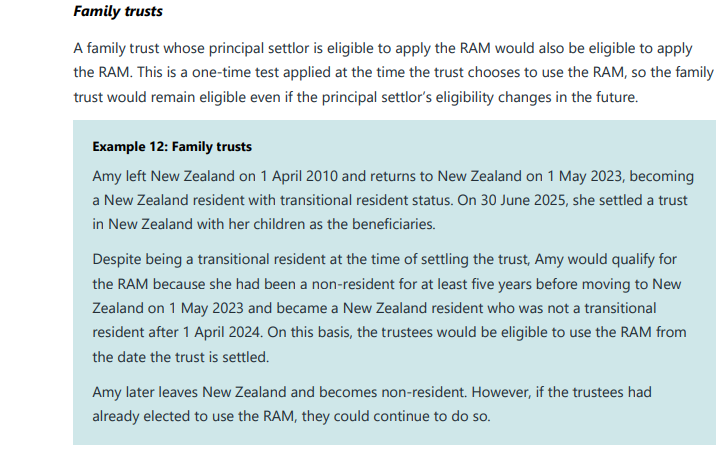

- a new calculation method for calculating foreign investment fund (FIF) income or loss from attributing interests in a FIF. The new revenue account method (RAM) would allow certain FIF interests to be taxed on a realisation basis – that is, on dividends derived and gains or losses on disposal. The following example on page 38 explains how this could work for a family trust:

- that an eligible person may apply the RAM to all foreign shares if they are generally liable to tax in another country on the disposal of those shares on the basis of their citizenship or a right to work and live in that country. This proposal (called “extended RAM”) would only apply if the person was subject to concurrent taxation in another country with which New Zealand has a tax treaty. A family trust would be eligible for the extended RAM if the principal settlor is also eligible for the extended RAM. However, if the principal settlor subsequently loses their eligibility for the extended RAM, then it is proposed that the family trust would transition out of the extended RAM regime to the ordinary RAM regime. For the purposes of determining the eligibility of a family trust for the extended RAM, the principal settlor may lose their eligibility for the extended RAM due to them not being subject to concurrent taxation or because of death. However, the family trust would not lose its eligibility for the extended RAM just because the principal settlor leaves New Zealand.

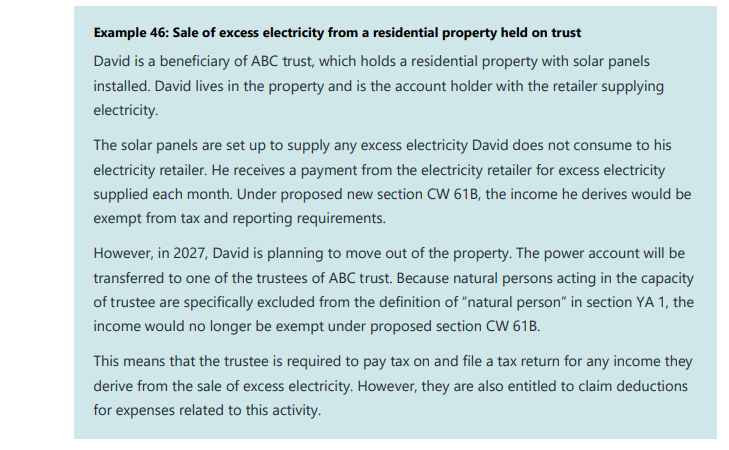

- a tax exemption for income derived by an individual from the residential supply of excess electricity. The exemption, whihc would be available to a beneficiary living in trust property, would not apply to the trustees. See the follwing example from the Bill Commentary:

- to exclude gratuitous payments to trustees from a deceased estate from the definition of pension income for the purposes of section CF 1 of the Income Tax Act 2007. As noted in the Bill commentary at p. 161:

References

thanks for this – much to consider as to practical effects.

Posted by David Marks KC | August 27, 2025, 12:27 am